“Once you start thinking about growth, it is hard to think about anything else”

Robert Lucas, 1995 Nobel Memorial Prize in Economics

It has been a busy year, probably the busiest since we founded Sprints a decade ago:

The only thing we have not managed is to keep pace with our investor letter writing. Henrik excuses himself by claiming discipleship to the French author Gustave Flaubert (of Madame Bovary), who believed that an ordinary, regular life was a prerequisite for vivid creation. Since 2025 was anything but ordinary, he blames the lack of creative writing on that.

“Uncertainty is not a fault of financial markets, but their defining characteristic”

Robert Shiller, 2013 Nobel Memorial Prize in Economics

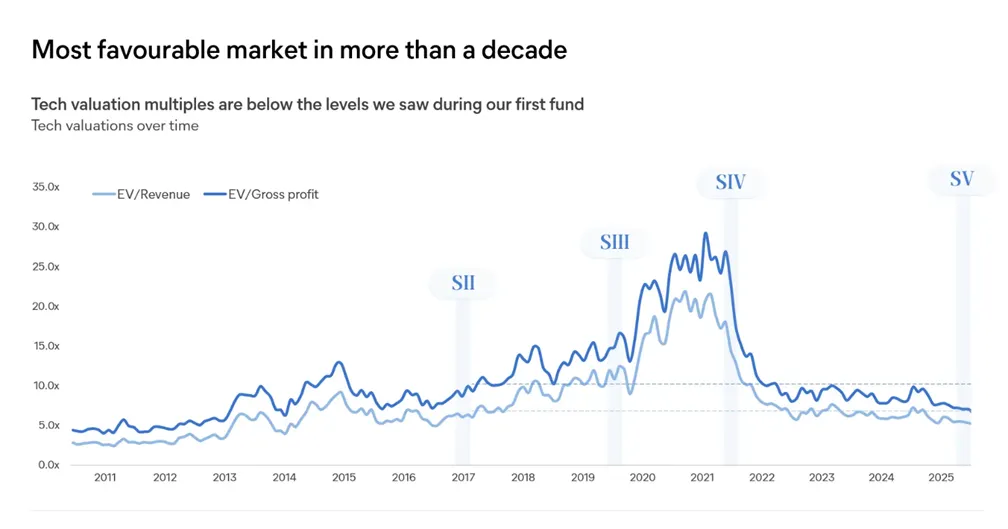

There are not many constants in tech. One candidate is the seemingly endless debate over whether we are in a bubble territory. At Sprints, we tend to observe this debate rather than actively participate in it – not out of lack of curiosity, but because confident macro forecasting lies outside our circle of competence. Our expertise is in evaluating individual companies and the durability of their qualities. By focusing on that instead of on macro, we have generated consistently strong returns over the last decades, throughout the market highs and lows.

Maybe tech is constantly in a boom-bust motion. And maybe that is a blessing rather than a curse. Maybe it makes the tech sector more resilient over time. To paraphrase the ‘bubble‑economist’ Hyman Minsky – long periods of apparent stability in markets are themselves destabilising, because people start to build around the belief that markets will remain static. This encourages risk‑taking, often in the form of increased leverage, which makes the inevitable correction much more dramatic and costly.

Expecting constant volatility, while doing our job of selecting and managing the highest‑quality companies, remains the best defence we have found against these swings.

We have just emerged from the recent Covid‑era volatility that ended with declining growth and falling valuation multiples. Despite this recent headwind, our three previous funds (Sprints II, III and IV) have performed well. Our latest fund – Sprints V – is already showing strong momentum.

Our companies are selected for their long-term compounding profit growth potential, which drives a similar fund performance over time. Sometimes – in the case of Sprints III and Sprints IV – temporary corrections in the market can create shallow J-curves. Other times – such as in Sprints II and V – the opposite happens and the funds show solid returns early on. Over time, they all have a high probability of meeting or beating our 3x return target.

Sprints' ambition, which is to deliver consistently strong returns, is grounded in the robust and durable profit growth of our portfolio companies. If any of our funds were publicly listed today, they would rank among the fastest‑growing, most profitable companies in the market. By comparison, the c. 1,400 companies that make up Europe’s broadest equity index (STOXX Europe TMI) are, on average, forecast to deliver 0% growth in 2025 with an EBITDA margin of 18%. Meanwhile, Sprints’ portfolios are expected to grow 35% with an EBITDA margin of 25%. When looking only at the listed European tech companies, this is unique. Even if we expand the universe to include European tech companies that are listed in the US, no company is growing faster than 30% year-on-year.

“In a dynamic economy, growth comes from firms that innovate and replace the old”

Philippe Aghion, 2025 Nobel Memorial Prize in Economics

What better time to deploy capital than when you have a proven investment methodology and the market is in a weaker cycle?

Over the last year we have invested EUR 560 million across Sprints IV, Sprints V and co‑investment vehicles. This represents almost one-third of all capital deployed since our first investment (Hemnet) in December 2016 – a great testament to the capabilities of our growing team. These investments closed the investment period for Sprints IV and launched Sprints V.

Our latest investments are exceptional companies that we have followed for many years, in some cases decades:

Willhaben is Austria’s leading classifieds marketplace, with entrenched positions in real estate and automotive. Its brand is comparable to prior portfolio winners such as Hemnet. We see significant upside in the product‑price mix as well as increased efficiency from modernising the tech platform.

Checkout.com is a leading modern payments platform serving many of the world’s largest and fastest‑growing tech businesses in high‑growth e‑commerce and digital verticals, such as Spotify, Netflix and Uber. It benefits from structural tailwinds in online payments and cross‑border commerce, with strong volume growth across its core markets. The business combines attractive growth with high incremental margins and a clear pathway to substantial profitability.

Flightradar24 is the global standard for real‑time flight tracking, with more than 55 million monthly active users, as well as a growing base of the largest airlines, airports, regulators and media customers. The company operates the world’s largest receiver network and a uniquely rich historical dataset, creating a strong moat in aviation data accuracy and reliability. Revenues are diversified across subscriptions, advertising and data packages, with attractive margins and robust cash generation. We see a multi‑year opportunity to serve the industry better and expand monetisation while remaining capital‑light.

Base (formerly BaseLinker) is the leading e‑commerce operating system for merchants in Poland, powering close to 40% of the Polish e‑commerce market while rapidly expanding internationally. Built over more than 15 years, Base has more than 30,000 customers. The platform is deeply embedded in merchant workflows across storefronts, marketplaces, logistics and invoicing, resulting in high stickiness and low churn.

Going forward, we currently see a larger number of opportunities in bootstrapped, profitable companies looking for the best partner for their next stage of growth. Many of the younger venture‑backed companies also look interesting but often combine lower gross margins with higher capital needs, a combination that history has taught us to be careful with. It is always easier to turn profitable in Excel than in real life.

The most attractive opportunity we see right now is to work with our portfolio, especially the four great companies we have just added to our roster. Our days are filled with company‑building work, and we believe there are several potential fund returners amongst the latest additions.

As outlined above, Sprints V is off to a strong start. The first close of the fund took place swiftly to allow us to complete the Willhaben investment in April and we have since welcomed a select number of new partners into our partnership. We are grateful to both existing and new partners for their support, which allowed us to bring this great portfolio of assets together in a short period of time.

The Sprints team has always maintained an ambition to significantly reinvest any exit proceeds received back into the funds. The continued liquidity generation from Sprints II will enable the GP commitment in Sprints V to exceed 10% of total fund size.

“Investments in human capital are the most valuable of all investments”

Gary Becker, 1992 Nobel Memorial Prize in Economics

Over the last twelve months we added significant resources to the value creation and operations teams. Sprints’ headcount has grown by one-third, with eight new colleagues. True to our hiring style, many of them are people we have worked with for years and whom we know to be world‑class at what they do.

Sprints now employs five former company CTOs as well as some of Europe’s most experienced recruiters for the tech sector. Among the new joiners are:

“The power of compound interest is extraordinary, but so is the power of compound learning”

Richard Thaler, 2017 Nobel Memorial Prize in Economics

With a low likelihood of a new investment before year-end, this feels like an appropriate moment to wish you all a happy holiday. Today, taking a break during the darkest and coldest weeks of the year is a luxury choice. Historically, winter meant a costly and dangerous period of forced hibernation. In Sweden, where this letter is being written, winter was a time where most occupations such as farming and fishing were impossible to conduct. Food was scarce to near desperate levels. It was a depressing and dangerous time.

The spread of electricity and artificial light fundamentally changed life in the North. Yet the transformation was slow. From invention, it took nearly half a century before electric light was brought to a majority of the Swedish population.

Today, the most advanced technologies – such as the latest AI tools and models – reach much of the global population within months. The digital revolution has not only generated higher returns and more wealth than any previous technological shift, it has also transformed our lives faster and more profoundly.

We live in the best world humanity has ever known. We have accomplished major achievements throughout history. But the current period of sustained technological progress is unique. What makes this era different?

One of this year’s winners of the Nobel Memorial Prize in Economics – Joel Mokyr – believes it is a knowledge revolution rather than a technology revolution that has “generated a continuous stream of new techniques,” as he described it in his book ‘The Lever of Riches’.

To tie Mokyr back to Flaubert, with the growing institutionalisation of Sprints, our New Year’s resolution will be to participate more actively in the creation, sharing and discussion of this knowledge flywheel through our website and our investor letters with more frequent updates on our companies and processes.

If Mokyr’s thesis is correct, participation in the exchange of ideas is as vital to economic progress as voting is to the health of a democracy. And just like in a democracy consensus is not required. Many of history’s most important innovations were initially dismissed by leading thinkers of their time. What matters is to participate so we generate and iterate as many ideas as possible. An added silver lining is that thinking and creating new ideas is likely the perfect antidote to the holiday boredom that we workaholics easily find ourselves in after a few days off.

Happy Holidays and Happy New Year!

Henrik and the Sprints Team

Stockholm, 19th December 2025